Staying above water: a systemic response to rising flood risk

This is the title of a recently published report from Marsh McLennan. It highlights the alarming rate at which flood risk is growing globally, estimating that currently 18% of the global population is exposed. Even limiting post-industrial average global temperature rises to 2oC could double that percentage.

The key message from the report is that given the lack of resilience to recent events, lead author Swenja Surminski argues that "society must urgently transform its approach to flood risk management."

She adds that flood risk management will play out along three areas:

- Learning to live with floods - building resilience to local-level, low intensity events.

- Building strategic protection - large scale interventions protecting critical assets, ensure financial resilience.

- Preparing for relocation - timely, equitable and financially sustainable resettlement.

Finally there is a discussion on enablers to make that transformation including transforming land use and infrastructure planning, mobilising financial capital and a shift to a resilience-focused insurance system.

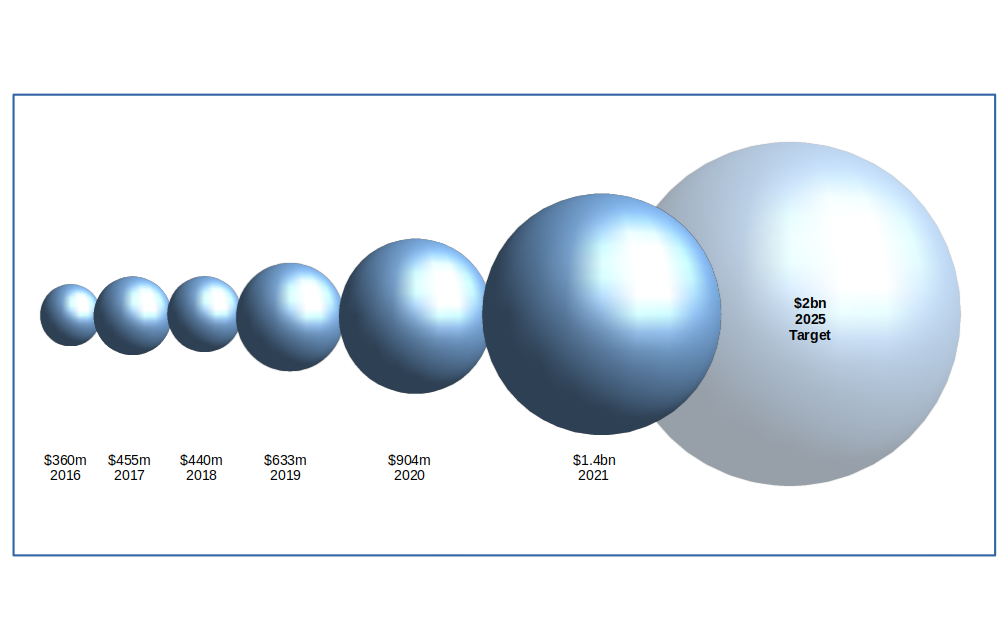

On those last two points, we discussed the insurance industry is uniquely set up to create impact and risk-adjusted returns 👇🏾

Sandy Jayaraj

Sandy Jayaraj

For sustainability professionals, understanding and relaying to the board that this is a strategic risk that requires consideration of how resilient a business is paramount. 'Resilience' after all is just 'sustainability' said with a different accent.

For homeowners, a working paper from CESifo made an interesting point about economic loss linked to climate change.

We are all familiar with the immediate loss from damage from the near-term occurrence of an actual disaster, but it is the loss of residential insurance that will likely be the first mechanism by which homeowners experience material economic loss directly attributable to climate change. Since mortgages are typically conditional on insurance (especially at the time of issuance), the withdrawal of residential insurance results in an immediate drop in property values.

In 2015, the (NZ) Parliamentary Commissioner for the Environment estimated that in some locations, a 10 cm sea level rise will turn what is currently a 1-in-100 year storm into an event that happens once in every 20 years.

Link to blog 👇🏾

Steven Bowen

This article featured in What Caught Our Eye, a weekly email featuring stories we found particularly interesting during the week and why. We also give our lateral thought on each one. What Caught our Eye is available to read in full by members.

If you are not a member yet, you can read What Caught Our Eye when it comes out direct in your email inbox plus all of our blogs in full...

Please read: important legal stuff.

{kind=link}