Sunday Brunch: Why (investors) need to care about food security

We know that food security is important for countries, but what about for investors? You might think that food is such a staple need for consumers that price almost doesn't matter - but that clearly isn't true. So what can investors do to enhance food security?

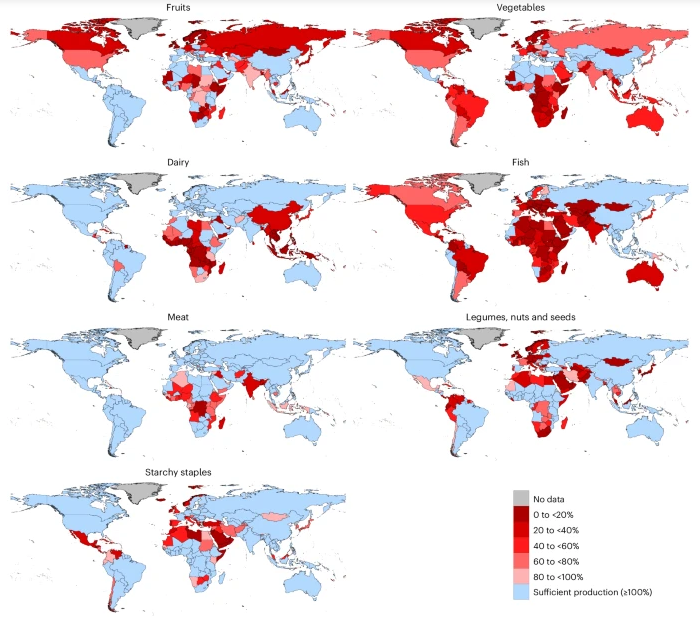

I recently came across a really interesting graphic in Visual Capitalist. Using data from a study published in Nature Food, it shows which countries are self sufficient in the seven essential food groups (starchy staples, fruits, vegetables, dairy, meat, fish, and legumes/nuts/seeds).

What is different about this work is that it doesn't just focus on calorie's.

The data shows that only one (small) country can produce all seven essential food groups domestically. And that many countries are only self sufficient in one. In the charts below, red is low self sufficiency and blue is fully self sufficient.

At a time when global supply chains are under threat, this feels like both a serious point and useful data.

As an investor, I can see a few issues with the analysis. First, country boundaries are a bit arbitrary with regard to food production, especially on continents. If your neighboring country has a surplus they can easily and willingly sell to you, you might not have a problem. This doesn't really undermine the analysis, it's just something we need to bear in mind.

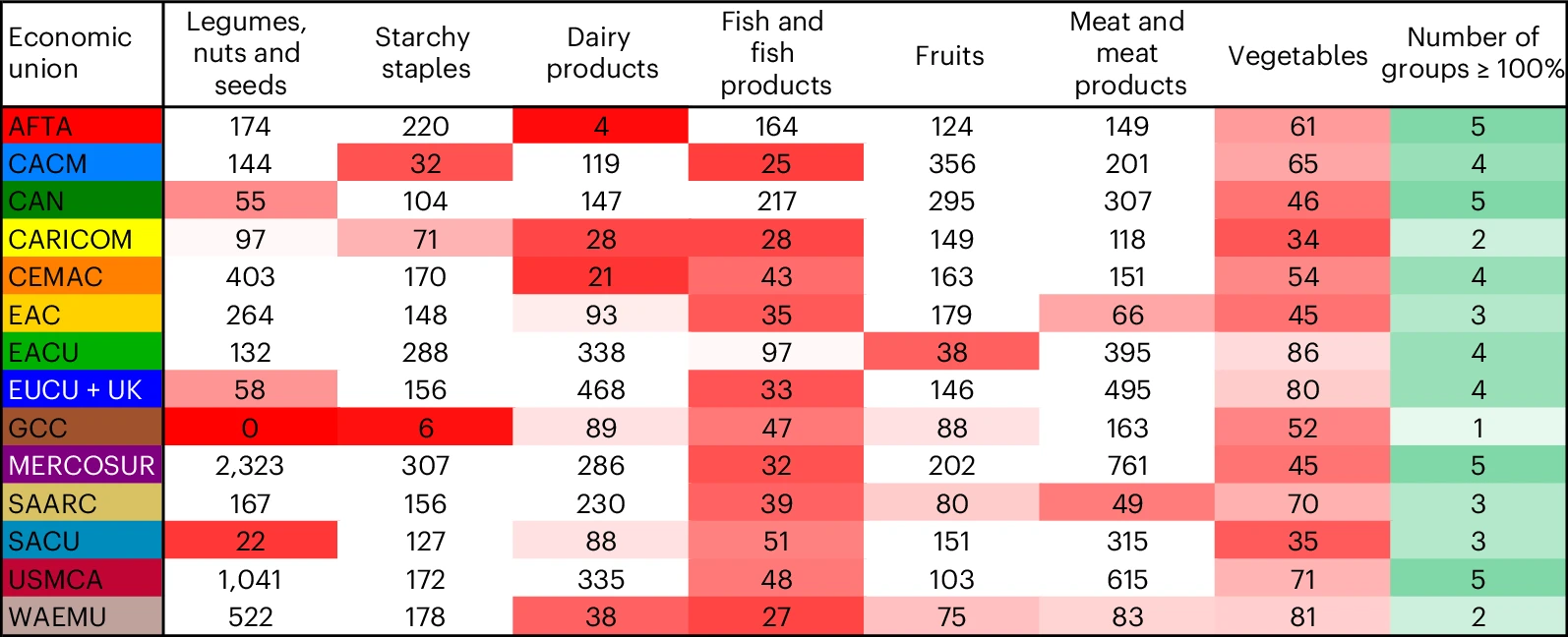

In fact the authors recognise this, and they have also done a similar chart at a regional level. In this case red is poor and green is strong.

Second, and perhaps more importantly, it lacks a forward looking perspective. If most of a regions fruit and vegetables (say) come from a country (or countries) that are facing future heat and/or water stress, then companies in the food supply chain could face material risks, unless they start to adapt now. We wrote about these risks in a recent blog - Fruit & vegetables and the very real climate risk.

The bottom line is that surging prices and excessive food price inflation are bad for nearly all companies in the food supply chains (yes, I know there are exceptions - mostly the traders and middlemen).

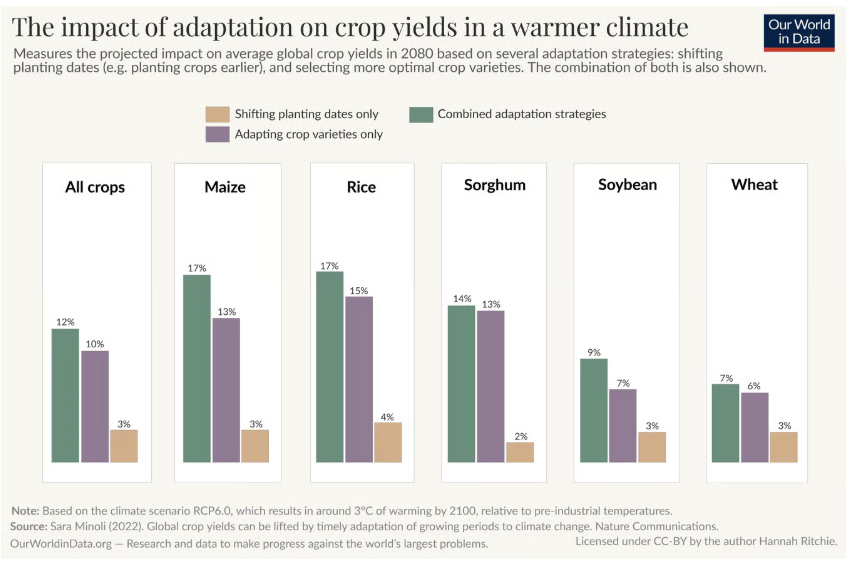

This is a topic that Hannah Ritchie at Our World in Data looked at back in 2024. In a three part series she examined the impact of climate change on food production so far, what we might expect in the future, and things we can do to adapt. It's this third instalment I want to include today.

What options do we have? Farmers can change what they plant. For instance they could shift from maize to wheat, or they could grow a different variety of the same crop. They can also change where they grow a crop. If temperatures rise or fall, crop production can shift north or southwards towards more optimal temperatures. In mountainous areas, it can move up and down the slopes. This is similar but slightly different to changing what they grow. Additionally, they can also change how crops are managed (irrigation etc) and when they plant.

These actions can make a real difference. The article highlights 2022 research by Minoli et al (Global crop yields can be lifted by timely adaptation of growing periods to climate change). The graphic below uses data from that research, showing that changing crop varieties and planting times can positively impact yield.

There is also a lot that can be done around irrigation, fertiliser use and other inputs (which the article also discusses).

But, if you think like me you may be wondering what this has to do with investors? After all, these are actions for farmers. And 'we' don't invest in farming. But is this really correct?

We have consistently argued over the years that farmers are often the least able to fund many of the required changes.

We should not under estimate the scale of the investment needed. A 2023 report from 25 leading philanthropies estimated that the cost of a global transition to agroecology and regenerative approaches is US$ 250-430 billion pa. But, they also highlight that this is just a fraction of the US$12 trillion pa of hidden costs, including include hunger and malnutrition, environmental damage, lost worker productivity, and health care.

And, at the risk of stating the blindly obvious, farmers normally cannot just up and move if their farm is becoming less and less financially viable. Plus shifting food production will generally require us to reconfigure supply chains - which means investments in food storage facilities and transport.

If not the farmers, then who needs to fund this. Governments can do a bit but mostly it's the food processing, and food retailing companies/supermarkets. They have materially more financial firepower (especially in their buying decisions.

And, it's also in their own financial self interest. Soaring food prices help no-one. By being a 'first mover' they can build barriers to entry and stronger brands. Consumers care about where their food comes from.

So maybe, just maybe, investors can help to keep the companies we invest in more profitable in the long run, and help with food security.

One last thought

Sometimes it's changing consumer demand patterns we need to watch, which can slowly alter what it is we eat. We know that ruminants (mostly cows) are responsible for a big chunk of our methane emissions. As investors, who should we expect to act to reduce this, and how? And if it's not companies, should they still prepare for a lower meat/dairy future?

Grant me the strength to accept the things I cannot change, the courage to change the things I can, and the wisdom to know the difference. Reinhold Niebuhr - a Lutheran theologian in the early 1930's

Please read: important legal stuff. Note - this is not investment advice.

%20need%20to%20care%20about%20food%20security){kind=link}