Where we end up with battery technology matters.

does battery technology matter, and are we worrying about the wrong raw material issues?

This is the third blog in the series on some of the key issues we need to consider in relation to EV's. This considers the question - does battery technology matter, and are we worrying about the wrong raw material issues? Because battery technology is changing & changing fast.

Last week the IEA published their 2024 Global EV outlook. This is significant for two reasons.

First, transport is a really important sector for decarbonisation. According to Our World in Data, transport accounts for around 20% of global CO2 emissions, with c. 75% coming from ground transport. So, a good problem to solve.

And second, it's importance comes from the fact that we have a solution that reduces transport emissions, one that we know works. Along with decarbonization of our electricity network, transport is the most investible 'green' theme.

That solution is obviously Electric Vehicles. We can build them at scale, they are getting cheaper, and, assuming we decarbonise electricity generation, they can make a real difference. But, it can be complicated.

We are sure you will have seen a lot of coverage of the report. So, rather than rehash a summary, we have picked three aspects where we think a bit of thought is needed.

These are - how do we expand EV's outside of the current three big markets - is this the decade of the Chinese mass market EV, what is happening on EV charging, and advances in battery technology. What links them all, as with most things to do with EV's, is China.

This blog considers Topic 3 : Can we produce enough batteries to met EV demand?

In topic 2 we talked about one barrier to mass market adoption of EV's - charging. That is largely a solvable challenge, if we have the political will and some investment support. The battery challenge is more difficult. We have highlighted in the past the need for more mining of what are known as critical minerals. Much more mining. But even here solutions exist, if we can get around the politics.

Steven Bowen

Steven Bowen

The IEA report sets out in a bit more detail the scale of the challenge.

The growth in EV sales is pushing up demand for batteries, continuing the upward trend of recent years. Demand for EV batteries reached more than 750 GWh in 2023, up 40% relative to 2022.

95% of the growth in battery demand related to EVs was a result of higher EV sales, while about 5% came from larger average battery size due to the increasing share of SUVs within electric car sales.

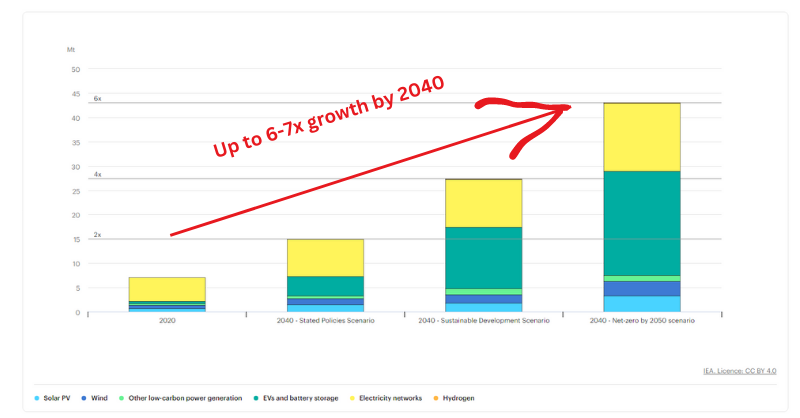

More batteries means more of some types of mining

More batteries means extracting and refining greater quantities of critical raw materials, particularly lithium, nickel and maybe cobalt.

Rising EV battery demand is the greatest contributor to increasing demand for critical metals like lithium and cobalt. Battery demand for lithium stood at around 140 kt in 2023, up more than 30% compared to 2022; for cobalt, demand for batteries was up 15% at 150 kt. EV's are important for these minerals, as they make up the majority of the current demand (85% and 70% respectively).

It's also similar, although to a lesser extent, in nickel. Battery demand for nickel stood at almost 370 kt in 2023, up nearly 30% compared to 2022. But batteries only make up 10% of total nickel demand.

Do we have enough battery production capacity? Yes

Interestingly, the future challenge is less about having enough battery production capacity. At least it is if we exclude politics.

Part of the reason is China. As the IEA highlights - in 2023 China used less than 40% of its maximum cell output. And cathode and anode installed manufacturing capacity was almost 4 and 9 times greater than global EV cell demand in 2023. They are making way more battery material than they need now, so it's no surprise that they are big exporters.

This imbalance is changing. In 2023, the installed battery cell manufacturing capacity was up by more than 45% in the United States, and by nearly 25% in Europe. If current trends continue by the end of 2024, capacity in the United States will be greater than in Europe.

And we might need less cobalt than we previously thought.

Cobalt is controversial. Much of it comes from the Democratic Republic of Congo, where human rights are an issue. It's a topic that comes up a lot. Critics of EV's say how can EV's be clean, when producing them involves human rights abuses. And sustainability professionals worry about how do you fix this?

Part of the answer is battery chemistry. Despite what you might have read, not all batteries contain cobalt. There is a battery type that uses no cobalt. Its called LFP (it stands for Lithium Iron Phosphate - the F is from the chemical symbol for iron - Fe).

Over the last five years, LFP has moved from a minor share to the rising star of the battery industry, supplying more than 40% of EV demand globally in 2023, more than double the share recorded in 2020. And some analysts expect it to be over 50% of demand very soon.

Why? because it's cheaper. Which is probably why LFP production and adoption is primarily located in China, where two-thirds of EV sales used this chemistry.

And looking further out, there could be a future for sodium-ion batteries. These batteries not only don't use cobalt, they don't use lithium either. The IEA estimates that sodium-ion batteries could be 20% cheaper, and so they could become the battery of choice for smaller urban EV's. It will not surprise you that the announced sodium-ion manufacturing capacity in China is estimated to be about ten times higher than in the rest of the world combined.

The other aspect that we need to think about is battery recycling, what some people call 'urban mining'. This could also help bridge some of the critical mineral gap.

👉🏾 The 5% rate and other untruths about battery recycling.

This article featured in What Caught Our Eye, a weekly email featuring stories we found particularly interesting during the week and why. We also give our lateral thought on each one. What Caught our Eye is available to read in full by members.

If you are not a member yet, you can read What Caught Our Eye when it comes out direct in your email inbox plus all of our blogs in full...

Click this link to register 👉🏾 https://www.thesustainableinvestor.org.uk/register/

Topic 3: Can we produce enough batteries to met EV demand?

In topic 2 we talked about one barrier to mass market adoption of EV's - charging. That is largely a solvable challenge, if we have the political will and some investment support. The battery challenge is more difficult. We have highlighted in the past the need for more mining of what are known as critical minerals. Much more mining. But even here solutions exist, if we can get around the politics.

Steven BowenThe IEA report sets out in a bit more detail the scale of the challenge.

The growth in EV sales is pushing up demand for batteries, continuing the upward trend of recent years. Demand for EV batteries reached more than 750 GWh in 2023, up 40% relative to 2022.

95% of the growth in battery demand related to EVs was a result of higher EV sales, while about 5% came from larger average battery size due to the increasing share of SUVs within electric car sales.

More batteries means more of some types of mining

More batteries means extracting and refining greater quantities of critical raw materials, particularly lithium, nickel and maybe cobalt.

Rising EV battery demand is the greatest contributor to increasing demand for critical metals like lithium and cobalt. Battery demand for lithium stood at around 140 kt in 2023, up more than 30% compared to 2022; for cobalt, demand for batteries was up 15% at 150 kt. EV's are important for these minerals, as they make up the majority of the current demand (85% and 70% respectively).

It's also similar, although to a lesser extent, in nickel. Battery demand for nickel stood at almost 370 kt in 2023, up nearly 30% compared to 2022. But batteries only make up 10% of total nickel demand.

Do we have enough battery production capacity? Yes

Interestingly, the future challenge is less about having enough battery production capacity. At least it is if we exclude politics.

Part of the reason is China. As the IEA highlights - in 2023 China used less than 40% of its maximum cell output. And cathode and anode installed manufacturing capacity was almost 4 and 9 times greater than global EV cell demand in 2023. They are making way more battery material than they need now, so it's no surprise that they are big exporters.

This imbalance is changing. In 2023, the installed battery cell manufacturing capacity was up by more than 45% in the United States, and by nearly 25% in Europe. If current trends continue by the end of 2024, capacity in the United States will be greater than in Europe.

And we might need less cobalt than we previously thought.

Cobalt is controversial. Much of it comes from the Democratic Republic of Congo, where human rights are an issue. It's a topic that comes up a lot. Critics of EV's say how can EV's be clean, when producing them involves human rights abuses. And sustainability professionals worry about how do you fix this?

Part of the answer is battery chemistry. Despite what you might have read, not all batteries contain cobalt. There is a battery type that uses no cobalt. Its called LFP (it stands for Lithium Iron Phosphate - the F is from the chemical symbol for iron - Fe).

Over the last five years, LFP has moved from a minor share to the rising star of the battery industry, supplying more than 40% of EV demand globally in 2023, more than double the share recorded in 2020. And some analysts expect it to be over 50% of demand very soon.

Why? because it's cheaper. Which is probably why LFP production and adoption is primarily located in China, where two-thirds of EV sales used this chemistry.

And looking further out, there could be a future for sodium-ion batteries. These batteries not only don't use cobalt, they don't use lithium either. The IEA estimates that sodium-ion batteries could be 20% cheaper, and so they could become the battery of choice for smaller urban EV's. It will not surprise you that the announced sodium-ion manufacturing capacity in China is estimated to be about ten times higher than in the rest of the world combined.

The other aspect that we need to think about is battery recycling, what some people call 'urban mining'. This could also help bridge some of the critical mineral gap.

Link to blog 👇🏾

Sandy Jayaraj

Please read: important legal stuff.

{kind=link}