Sunday Brunch: electrification - start with the viable applications

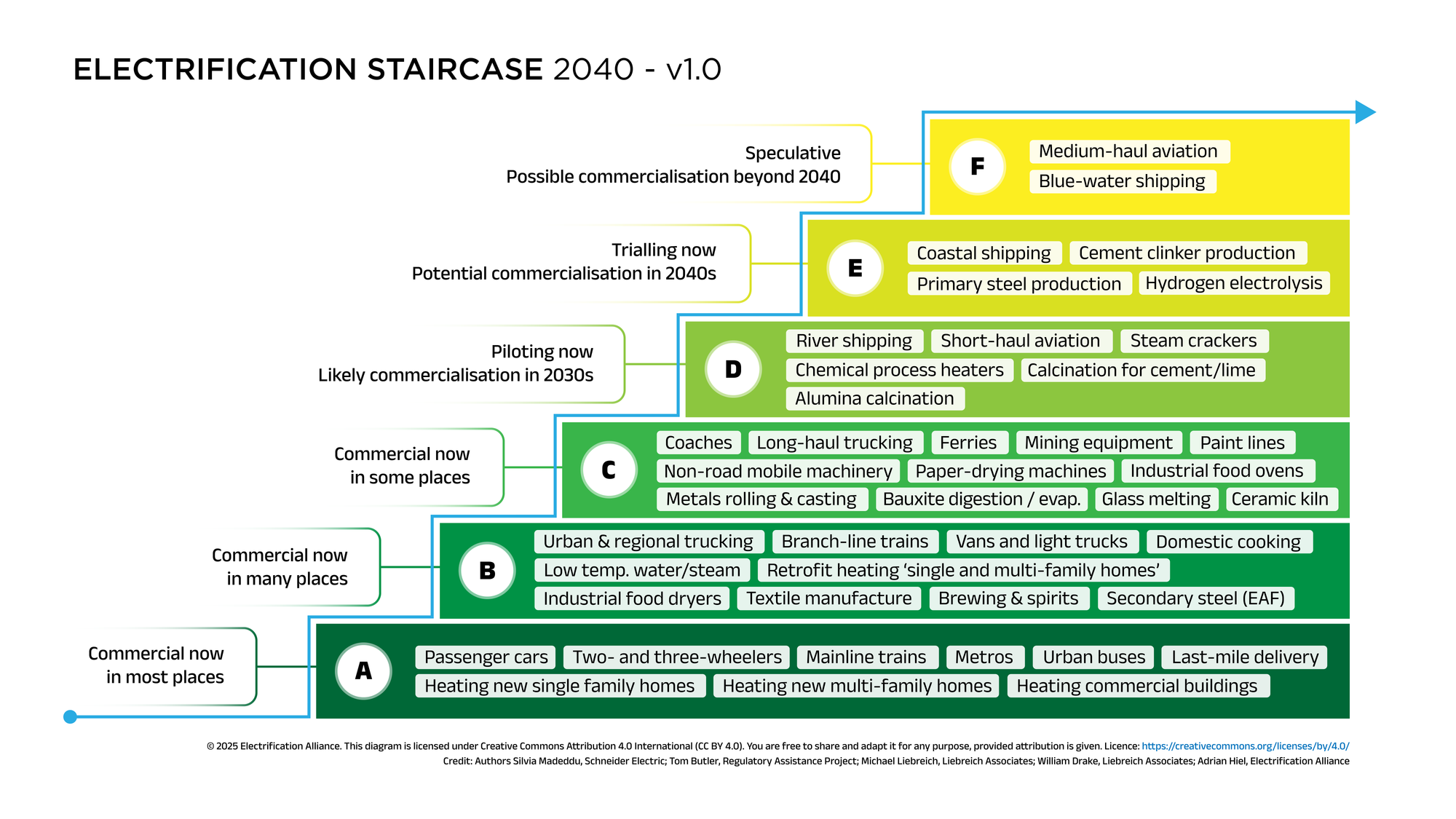

We often hear the phrase 'electrify everything' - a key element in getting us to net zero. But not all electrification solutions are financially viable. What should investors focus on? Michael Liebreich & team have come up with a handy 'ladder'. Which you invest in depends on your time horizon.

Last week we talked about sustainability narratives, the influence of how we see the world, and the weakness's of 'the market will fix it' story.

Today I want to talk about where the market driven narrative can actually work, specifically in relation to the electrification of our uses of energy.

To quote Liebreich "It is a truth universally acknowledged that all roads to a future of clean, affordable, resilient and abundant energy must run through the valley of deep electrification."

Or as others put it more succinctly 'electrify everything'. Which is great if your remit is policy, but as an investor it raises a simple (but material) question.

Where to start?

It's important to be honest, despite what you might read not all electrification solutions are ready to be rolled out at scale - the technology is not yet mature. And some of them are not commercially viable, although they may become so in the future. And a third group work in some places, but not in others.

As investors we are likely to be least interested in the solutions that are a distance away from being technically viable. And cautious about those that are not close to being commercial.

But which opportunities fit in which box?

Fortunately Michael Liebreich & team (including Dr Silvia Madeddu), have begun the process of making sense of this all. I say begun as this is the first cut, and as with the original hydrogen ladder, amendments are welcome.

From an investor perspective, it's application is relatively simple. Solutions in row A are already both technically and commercially viable. Which makes them more financially 'certain'. Row B solutions are already working in many places, and could reasonably be expected to get wider traction over time. These rows include electric vehicles and home/office heating plus some low heat industrial processes.

Taken together these can be thought of as our safe (in an investment sense) solutions. Although of course we still need to do a full investment analysis before we decide if the price is right for us.

Rows C & D is where it starts to get more interesting. These are solutions that are likely (but not certain) to become technologically and financially viable in the next decade. Row C works now, but only in some places. And row D solutions are still at the pilot project stage. A reasonable chunk of these rows involve industrial processes (hence my reference above to Dr Silvia Madeddu - who is an expert in industrial heat applications).

Row's E & F are (from an investor perspective) long shots, or perhaps more strictly investments for those with a longer time horizon and a specific risk tolerance. You will see that this includes cement clinker production (for concrete) and primary steel (in simple terms not the reprocessing of scrap steel via an electric arc furnace).

It goes without saying that this use of the staircase is a simplification, and further detailed analysis is needed. But it's a great start, a really useful sieve to help companies and investors to focus in on the solutions that stand the best chance of success. And for policy makers to see where action can have the greatest impact.

And to be clear, nothing in this formulation suggests we should ignore the solutions in the top rows. Some are material GHG emitters and are worthy of detailed study. But, we need to do so knowing that it's going to take time, and the financial risks are higher.

And for those who haven't yet read the team's explanation of the staircase (or listened to the podcast), it's about end use solutions, and so it doesn't include investments in electricity generation and transmission networks (an important topic in it's own right but one that we are closer to understanding).

One last thought

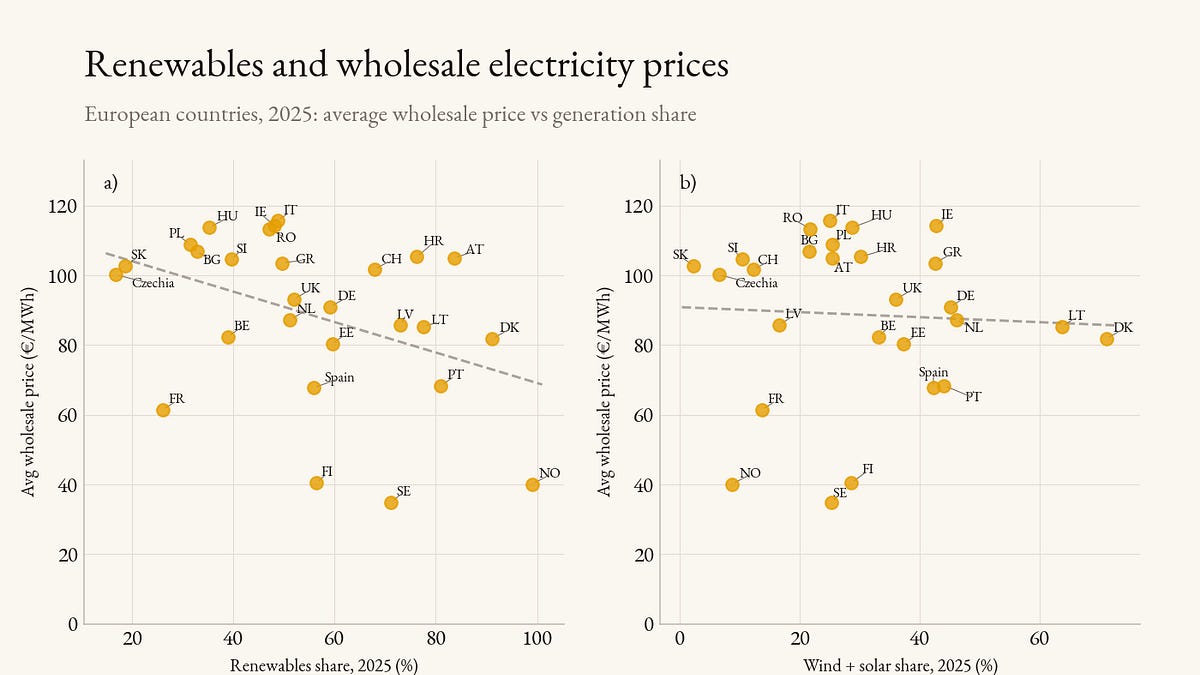

One important driver of this process is electricity price. And by electricity price we often mean the price to the consumer (retail or industrial). Jan Rosenow, a Professor at Oxford University, has done some interesting work on how this price is set, and how the retail price is often set by costs unrelated to the generation process, including who pays the network costs.

To quote his recent substack post ...

In many cases, the non-energy components of the electricity bill are responsible for unhelpfully large electricity to gas price ratios. In the second half of 2025, the average European household paid roughly 2.5 to 3 times more for a unit of electricity than for the same energy delivered as gas.

Grant me the strength to accept the things I cannot change, the courage to change the things I can, and the wisdom to know the difference. Reinhold Niebuhr - a Lutheran theologian in the early 1930's

Please read: important legal stuff. Note - this is not investment advice.

{kind=link}